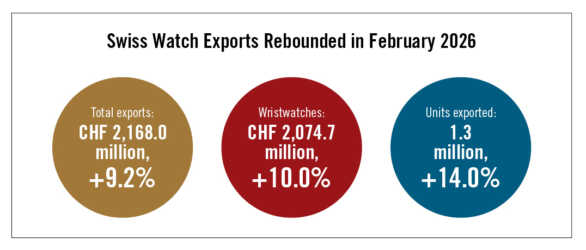

Swiss watch exports found their footing again in February 2026, posting a 9.2% year-over-year increase to CHF 2.168 billion after what the Federation of the Swiss Watch Industry described as a lacklustre start to the year. The rebound was helped in part by a favourable comparison base, but the bigger story was the strength of three major markets: the United States, Japan and France.

For jewellers, distributors and watch retailers, that matters because February did not simply deliver a better headline number. It also showed where the real energy is returning in Swiss watchmaking and where pressure continues to build. Wristwatch exports reached 1.3 million units, up 14.0%, while wristwatch value rose 10.0% to CHF 2.0747 billion. Other watch products, however, declined 6.2%, reminding the trade that this was a selective recovery rather than a broad-based surge across every category.

The rebound was real, but it was not universal

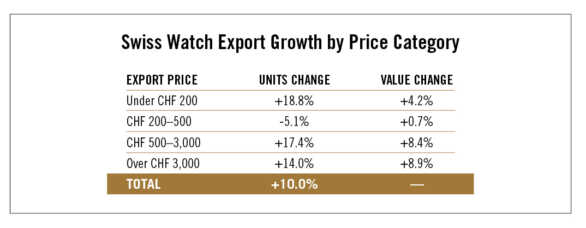

The most important takeaway from the February figures is that Swiss watch exports are growing again, but not evenly. FH said watches priced above CHF 500 at export were the main growth driver, with the strongest momentum concentrated in the CHF 500 to CHF 3,000 segment and in watches above CHF 3,000. That is a meaningful signal for the trade because it suggests demand remains healthiest where brand equity, product story and margin structure are stronger.

That pattern also fits the broader context of 2025. FH’s annual review said Swiss watch exports fell 1.7% last year to CHF 25.6 billion, marking a second consecutive annual decline, while the industry faced uncertainty tied to U.S. trade policy, weakness in China and Hong Kong, and higher costs linked to record gold prices and a strong Swiss franc. In other words, February was encouraging, but it followed a difficult backdrop rather than a clean reset.

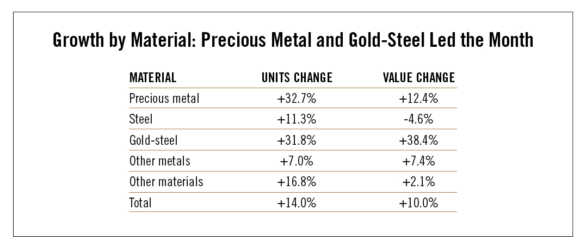

Materials told a deeper story than the headline

One of the more revealing aspects of the February data is what happened by material. Precious-metal watches rose 12.4% in value to CHF 804.1 million, while gold-steel or bimetallic models surged 38.4% to CHF 436.3 million. Steel watches moved in the opposite direction: volumes climbed 11.3%, but value fell 4.6% to CHF 639.3 million.

That split is worth watching closely. It suggests that units are moving in steel, but not with the same value performance as higher-end or more elevated material mixes. For retailers, that can point to a market where consumers are still buying, but where price architecture, product positioning and perceived prestige are doing more of the heavy lifting than simple category volume. That is an interpretation based on FH’s material and price-segment data rather than a direct statement from the federation.

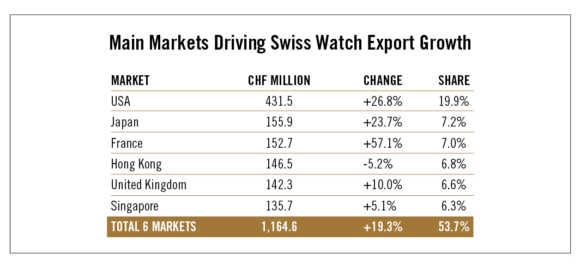

The United States stayed decisive, while Asia remained uneven

The United States was again the biggest force behind the month, rising 26.8% to CHF 431.5 million and accounting for 19.9% of February export value among the listed main markets. Japan climbed 23.7% to CHF 155.9 million, while France jumped 57.1% to CHF 152.7 million. FH said France’s sharp rise likely reflects transit to other destinations rather than a sudden jump in domestic demand.

Not every market joined the rebound. Hong Kong fell 5.2%, and FH said China was down 11.0%, signalling that the region’s weakness has not been solved by one better month elsewhere. Europe, meanwhile, was mixed: France and the United Kingdom posted gains, but Germany and Italy remained negative. Singapore rebounded 5.1%, and the United Arab Emirates was described as steady at 5.1% growth at that point in the period covered.

This lines up with FH’s 2025 annual assessment, which found Asia down 3.8% for the year and said exports to China had fallen by more than one-third over two years. The American market, by contrast, remained the sector’s leading destination and showed signs of resilience even in a volatile environment.

What Canadian jewellers should take from the February numbers

For Canadian jewellers, the February report is best read as a sign of selective strength, not blanket recovery. Premium Swiss watch demand is still present. The U.S. remains critical. Japan has regained momentum. France’s spike needs to be treated carefully because FH itself says the increase may reflect re-export or transit flows. At the same time, China and Hong Kong continue to drag on the global picture.

The practical lesson is clear: retailers should pay closer attention to brand power, material mix and where value is being created. February favoured better-priced Swiss products, especially above CHF 500 export price, while steel’s weaker value result showed that more units do not automatically mean stronger revenue performance. For stores planning watch assortments, this is a reminder that the market is rewarding confidence at the premium end, but still punishing softness in weaker geographies and more price-sensitive segments.

One more caution matters. FH explicitly states that its figures reflect exports, not sell-through to end consumers, and that the data are consolidated across all Swiss watch companies rather than representing the performance of any individual brand or group. That distinction is essential. Export growth can point to improving confidence in the trade, but it is not the same thing as proof that consumer demand is accelerating at retail at the same rate.

For now, February 2026 delivered welcome relief for Swiss watchmaking. But it also reinforced a message the industry has been living with for some time: growth is available, just not everywhere, and not for everyone.

FAQ

Did Swiss watch exports grow in February 2026?

Yes. Swiss watch exports rose 9.2% year over year in February 2026 to CHF 2.168 billion.

Which markets drove Swiss watch export growth in February 2026?

The strongest contributors were the United States, Japan and France, with gains of 26.8%, 23.7% and 57.1% respectively.

Were all markets strong in February 2026?

No. Hong Kong declined 5.2%, China fell 11.0%, and Europe was mixed despite strong results in France and the U.K.

Which Swiss watch segments performed best?

FH said watches priced above CHF 500 were the main growth driver in February, while precious-metal and bimetallic watches were especially strong.

Sources

Federation of the Swiss Watch Industry FH, Swiss watchmaking in February 2026. (FH Swiss)

Federation of the Swiss Watch Industry FH, Watch industry statistics. (FH Swiss)

Federation of the Swiss Watch Industry FH, Swiss watch exports in 2025. (FH Swiss)

Reuters, Swiss watch exports return to growth in February before Middle East conflict, March 19, 2026. (Reuters)

Swiss SME Portal / SECO, Watchmaking industry remains under pressure, February 11, 2026. (Federal Dept of Economic Affairs)